Getting a tax refund is always a pleasure. Paying a credit card or other debt, investing your income in the market, or investing in a pension fund are just a few of the ways you can use your tax return. From paying high-interest rates to investing in a company or savings for retirement, there are many ways to make the most of your repayment. One or more of these options may be perfect for you.

From paying high-interest rates to investing in a company or savings for retirement, there are many ways to make the most of your repayment. One or more of these options may be perfect for you. Your tax return is a great opportunity to prepare for the future.

Of all the options you have before, you might be best off deciding to use it to pay off your existing debt but read on to learn more about how your tax return can work.

Create Next Year’s Tax Credit

Here’s how to use your tax return to create a refund for the next year. If your combined tax rate is 35% (e.g. 28% for federal, 7% for the state of residence), you can generate a $1,050 refund next year by transferring your $3,000 refund to your existing tax-protected IRA account. Anything you add here is a bonus.

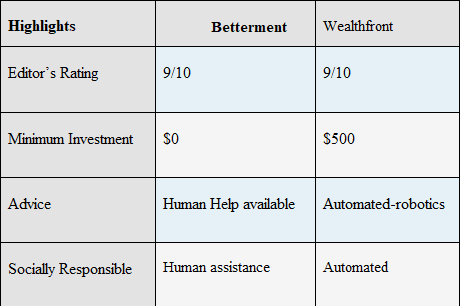

The IRA’s money will also increase excluding taxes. Especially if you’ve been investing in this IRA for decades, you can invest in a way that increases multiple times compared to your initial investment. You can open an IRA with a robotic consultant like Betterment or Wealthfront. Both services are recommended by us for a safe future investment. Both services have low fees and can start at as little as $500 (Wealthfront) or $0 (Betterment). Below is a small comparison between the two:

Invest in S&P 500 Index Fund

Since 1950, the S&P 500 has provided an average annual salary of around 11% including dividends. If you invest in an index fund like the Vanguard 500 Index Fund ETF (VOO) with a redemption amount (e.g. $3,000), you can turn your small investment into $24,187 in just 20 years with an annual return of 11%. This is an 8-fold increase in your investment.

That doesn’t mean you’ll get an 11% annual return on investment like receiving a security deposit (CD) or government bond. However, you can view this as the average effective interest rate over several decades.

One of the biggest characteristics of index funds is their low cost and tax efficiency. Since index funds are based on the underlying index, they are traded only in response to changes in the index itself. This means the transaction cost is very low. For the same reason, funds do not generate as many taxable capital gains. They are not very different from the tax protection pension system, they just grow and grow.

To invest in index funds, you need to choose the right broker. I love the Ally Invest and Vanguard online platforms because of their low fees and excellent fund options.

Put It In a High-Yield Savings Account

Competition between online banks is very high, and this is good news for money. Many of these financial institutions have cut the cost of owning hundreds of existing branches, so you can pay much more interest. This makes saving money much easier on rainy days.

Depositing money into U.S. savings accounts can be a particularly insightful idea, as most of these accounts have FDIC insurance up to $250,000. This way, even if your bank goes bankrupt, your money is protected up to that amount.

Most of the banks we reviewed offer high-yield accounts. In particular, Ally Bank (Sister Ally Invest) is shining. Fees, deposits, and interest rates are above 2.00%.

Money market accounts are also of great value. It requires a higher minimum balance and a larger initial deposit than a regular savings account but usually offers higher interest payments. For example, if you can invest $10,000, you can earn 2.00% on Capital One 360’s Capital Markets account.

And don’t forget the proof of deposit (CD). They may ask you to set your money aside for some time, but this can be the highest paying bill. Currently, Barclays’ five-year CD produces more than 3.00% per year.

Pay Off Your Credit Card Debt at High-Interest Rates

If you have high-interest credit card debt, repayment should be your “first investment,” says Cynthia Meyer, Certified Financial Planner at Financial Finesse. This is because the return on money equals the interest rate, it is safe and risk-free.

For example, if your credit card has an interest rate of 24%, every dollar you pay to pay off your debt will effectively generate a return of 24%. This is far more likely than not to come to the market.

Would you like to pay off other debts like student loans, mortgages, or car bills? Pensioners may want to repay their mortgage before retiring.

Consider whether your profits will be better used to pay off credit or other debts. Federal student loan and mortgage rates average less than 10%.23 In both cases, tax incentives may apply. Paying off the debt with the highest interest rate makes more sense because it can reduce your total payment.

HSA Funds

If you have a health insurance plan that can be deducted into your Health Savings Account (HSA), you can keep the dollar there or invest in a better way. The HSA is tax-free three times. The money goes in before tax via payroll deductions (or tax-free if you invest directly). Withdraw money as long as you use it, you are tax-exempt and tax-free.

This means you can save about 25% on all medical expenses by transferring money you use for a short period through your account. You can also invest in your account to grow it. By the age of 65, withdrawals not used for treatment are considered a 401(k) deduction and are taxed at the current income tax rate.

The subsidy limit for these accounts is $3,550 for individuals and $7100 for families by 2020. 4. By 2021, these figures will increase to $3,600 and $7,200 respectively.

According to Meyer, “If you haven’t emptied your HSA donations for a year, you can increase your salary and invest in a wide range of stock market funds. It’s much better than the Roth IRA because it’s pre-tax and tax-free growth”.

Contributing to the IRA

If your workplace retirement plan already meets your requirements or does not exist, the IRA is the next step in preparing for retirement. However, you have to choose between a Roth IRA and an existing IRA. There is an important difference between the two.

You get a deduction in advance for the money you put in the traditional IRA 5. It increases with a tax deferral, but you pay income tax when you start withdrawals (you can do it from 59 and a half years old, you should do it after 70 1/2 1/2 years). Today there are no tax credits at the Roth IRA, but opening a retirement account is tax-free.

According to Meyer: “Roth [IRA] is generally reasonable if you think your retirement period will be the same or higher.” No need to withdraw Roth either. That means you can send money to your heirs and you have great flexibility. In many cases, you can withdraw money without penalty for paying for your child’s college tuition or at home.

Increase your 401(k) Contribution

Add your tax refund to your daily expenses and increase your donation to 401(k). If you only invest 3% of your salary and your business is up to 6%, you can double your pre-tax investment income to maximize your pension fund.

Wages are slightly lowered, but rebates can be used as compensation for pension investments and reduced taxable income.

Conclusion

Think carefully about what you will do with your tax return. You can really have a great time. However, you can spend money on areas that can improve your finances, and sometimes you can use it for years to come.

Enjoyed this blog? Make sure to check out our other contents!